Reserve fund study

Reserve Funding Justification

The Board has indicated that reserve funding levels should exceed 50%. However, the Association’s principal long-term obligation is road maintenance that historically has been funded through the annual general operating budget. Members may reasonably request further explanation before any dues increase absent supportive engineering studies, reserve analysis or documented capital replacement schedules.

What is Reserve?

If an HOA board fails to comply with the following:

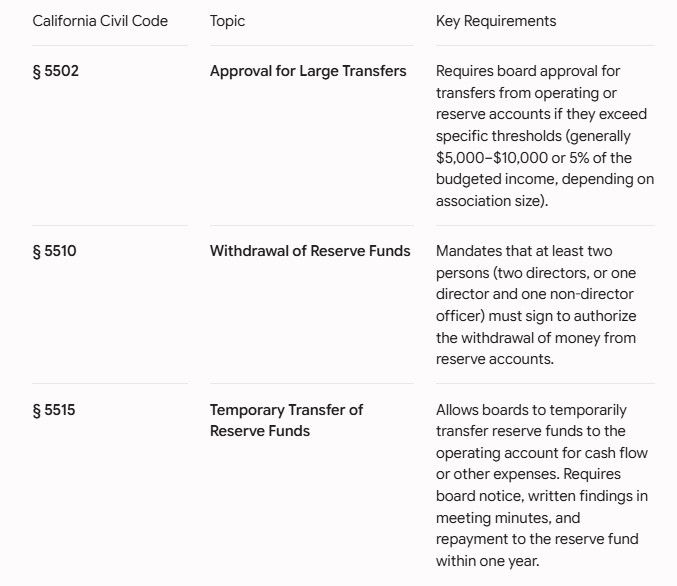

1) Civil Code 5510 (monthly financial reviews),

2) Civil Code 5515 (reserve fund transfer rules) and

3) Civil Code 5502 (For 51 or more units: Prior written approval is required for any transfer greater than the lesser of $10,000 or 5% of the annual budget)

The penalties aren't usually a "fine" paid to the government, but rather severe legal and financial consequences triggered by homeowners or the courts.

Here is what can happen if the board ignores these rules:

1. Lawsuits for Breach of Fiduciary Duty

The biggest risk is a lawsuit. Board members have a "fiduciary duty" to act in the best interest of the association.

-

Negligence: If a board fails to review the books (5510) and an employee or management company embezzles money, the board can be held personally liable for negligence because they weren't watching the funds as required by law.

-

Loss of "Business Judgment Rule" Protection: California law usually protects board members from personal liability if they make a mistake in good faith. However, if you clearly break a specific law (like 5510 or 5515), a judge may rule that you did not act in good faith, meaning board members could be on the hook for damages personally.

2. Civil Penalties (Up to $500 per violation)

While the Davis-Stirling Act doesn't list a specific "fine" for 5510/5515, homeowners can sue in Small Claims Court for "records non-compliance" or "failure to follow procedures."

-

Under related codes (like Section 5235), if a homeowner asks to see the financial reviews the board is supposed to be doing and the board can't produce them, a court can award the homeowner up to $500 per violation.

-

The court can also order an injunction, which is a legal mandate forcing the board to start following the law immediately.

3. Payment of Attorney’s Fees

This is often the most expensive "penalty." In California HOA disputes, the "prevailing party" (the winner) is usually entitled to have their attorney's fees paid by the loser.

-

If a homeowner sues the board for not following financial codes and wins, the HOA (and potentially the board) will have to pay for the homeowner’s expensive lawyers. This can cost tens of thousands of dollars.

4. Removal from the Board

Persistent failure to follow financial laws is one of the most common reasons homeowners start a Recall Petition. Under the association’s bylaws and the California Corporations Code, members can vote to remove the entire board for failing to fulfill their duties.

5. Increased Insurance Premiums or Loss of Coverage

HOAs carry Directors and Officers (D&O) Insurance to protect the board. If an insurance company finds out the board is systematically ignoring state financial laws (5510/5515), they may:

-

Refuse to cover a legal claim.

-

Cancel the policy entirely.

-

Substantially increase the association’s premiums because the board is seen as a "high risk."

California Civil Code Section 5515 is part of the Davis-Stirling Common Interest Development Act, which governs Homeowners Associations (HOAs) in California.

This specific section addresses the transfer of funds from an association’s reserve accounts to the operating account.

Key Provisions California Civil Code Section 5515

-

Temporary Transfers: The board of directors may authorize the temporary transfer of money from a reserve fund to the association’s general operating fund to meet short-term cash flow requirements or other expenses.

-

Notice to Members: Before making the transfer, the board must provide notice of the intent to consider the transfer in a board meeting agenda.

-

Repayment Requirement: The transferred funds must be restored to the reserve fund within one year of the date of the initial transfer. However, the board can vote to delay the restoration if they determine that a delay is in the best interest of the association.

-

Written Findings: If the board decides to transfer the funds, they must explain the reasons for the transfer and how the money will be repaid in the board meeting minutes.

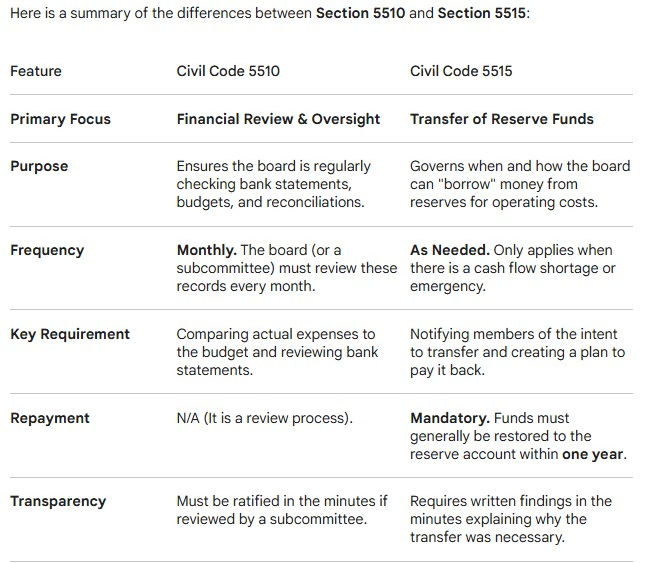

Key Provisions California Civil Code Section 5510

This covers the Board of Directors' review of financial records for a homeowners association. It is a critical part of the Davis-Stirling Act because it establishes the fiduciary duty of the board to stay informed about the association’s financial health.

Under this section, the board must review several specific financial documents on at least a monthly basis:

Required Monthly Reviews

-

Operating Accounts: A current reconciliation of the association’s operating accounts.

-

Reserve Accounts: A current reconciliation of the reserve accounts.

-

Actual vs. Budget: The current year’s actual operating revenues and expenses compared to the current year’s budget.

-

Bank Statements: The latest account statements prepared by the financial institutions where the association has its operating and reserve accounts.

-

Income and Expense Statements: An income and expense statement for the association’s operating and reserve accounts.

-

Check Register: The check register, monthly general ledger, and delinquent assessment receivable report.

Key Requirements for the Board

-

Frequency: These reviews must occur every month.

-

Individual or Group Review: The law allows these requirements to be met by a subcommittee of the board (such as a treasurer and one other officer) or by the full board during a meeting.

-

Ratification: If a subcommittee performs the review, the full board must ratify (officially approve) those actions at the next open board meeting and record that ratification in the minutes.

Why This Law Exists

Section 5510 is essentially a "checks and balances" rule. It prevents financial mismanagement or fraud by ensuring that the board cannot claim ignorance if funds go missing or if the association overspends. It forces transparency and consistent oversight of the community's money.

While both sections of the California Civil Code 5515 & 5510 deal with HOA financial transparency, they focus on two different responsibilities of the Board of Directors: oversight versus action.

Here is a summary of the differences between Section 5510 and Section 5515:

In Simple Terms:

-

Section 5510 is about watching the money. It forces the board to look at the books every month so they know exactly where every dollar is going.

-

Section 5515 is about moving the money. It sets strict "borrowing" rules so the board doesn't accidentally drain the reserve fund (the association's long-term savings) to pay for short-term daily bills without a plan to put it back.

Both codes work together to ensure that an association remains solvent and that the board is held accountable for the community's financial health.

California Civil Code Section 5502 is the "Large Transfer" law. It acts as a safety valve to prevent management companies or single board members from moving large sums of money without the full board's knowledge.

While 5510 is about watching the money and 5515 is about borrowing from reserves, 5502 is about authorizing any significant movement of funds.

Key Provisions of Section 5502

This code states that transfers cannot be made from an association’s reserve or operating accounts without prior written board approval if the amount exceeds certain limits.

The limits are based on the size of your association:

-

For 50 or fewer units: Prior written approval is required for any transfer greater than the lesser of $5,000 or 5% of the annual budget.

-

For 51 or more units: Prior written approval is required for any transfer greater than the lesser of $10,000 or 5% of the annual budget.

Why This Code Exists

Before this law was strengthened (around 2019 and updated in 2022), it was easier for a rogue board member or a management firm to move large amounts of money electronically without a formal vote. Section 5502 ensures:

-

No "Auto-Pilot" for Large Checks: Even if a large bill is legitimate (like a major roofing project), the board must specifically sign off on that high-value transfer in writing.

-

Fraud Prevention: It stops the "empty the account" scenario by requiring a paper trail for any movement of money that hits those $5,000 or $10,000 thresholds.

How it Works with 5510 and 5515

Think of it as a three-step financial security system:

-

5510 (The Eye): You look at the bank statements every month to see what happened.

-

5502 (The Gate): You must give written permission before a big chunk of money leaves the gate.

-

5515 (The Bridge): You follow special rules if you are moving money from the "Reserve" side of the gate to the "Operating" side of the gate.

If a board is paying a contractor $15,000 for a repair, they must follow 5502 to authorize that specific payment. If they are taking that $15,000 from the Reserve fund because the Operating fund is empty, they must also follow 5515.

a Property Owners Association (POA) is governed by the Davis-Stirling Act, these two sections are not "pick and choose" options; they are both mandatory requirements.

Here is why a POA generally cannot practice one without the other:

1. They are Part of the Same Legal Framework

Both Civil Code 5510 and 5515 belong to the Davis-Stirling Common Interest Development Act. If your association (whether called a POA or an HOA) manages a common interest development in California, it must follow the entire act.

-

Section 5510 is the Mandate: It requires you to watch the money every month.

-

Section 5515 is the Exception: It tells you the only legal way to "borrow" that money if the monthly review shows you're short on cash.

2. The Logic of the Law

The law is designed so that 5510 "triggers" the need for 5515:

-

By performing the monthly financial review (5510), the board realizes, "We don't have enough money in the operating account to pay the insurance bill this month."

-

Because they found this problem through 5510, they must then use the transfer process (5515) to legally move money from reserves to cover it.

3. Fiduciary Duty Risks

If a board chooses to follow 5510 (reviewing the books) but ignores 5515 (moving money without notice or a repayment plan), they are technically violating their fiduciary duty.

-

Practicing 5510 but not 5515 would look like a board that knows the finances are a mess but is moving money behind the scenes without the required transparency and member notice.

When would 5515 not be "practiced"?

The only way an association would "practice" 5510 but not 5515 is if they never need to borrow from reserves. * If the association is perfectly funded and the operating account always has enough money for bills, they will fulfill 5510 every month by reviewing the statements, but they will never have a reason to trigger the 5515 transfer rules.

The Bottom Line: You cannot "opt-out" of Section 5515 if you are moving money from reserves to operations. Doing so would leave the board vulnerable to legal challenges from homeowners for lack of transparency and failure to follow state-mandated financial procedures.

It's important to approach discussions about homeowners' associations (HOAs) and their financial practices with a balanced perspective. While there have been cases of mismanagement or misuse of funds in some HOAs, it's not accurate to generalize that all HOAs intentionally keep reserve funds high to manipulate money for private interests. Reserve funds serve a critical purpose in maintaining the long-term viability and stability of the community. However, I can provide an overview of the factors that might lead to concerns about financial mismanagement in HOAs:

1. Lack of Transparency: In some instances, a lack of transparency about the financial decisions and actions of the HOA board can lead to suspicions about their intentions. When homeowners feel that they don't have access to information about how the reserve funds are being managed and utilized, it can create distrust.

2. Limited Accountability: If the HOA board lacks accountability mechanisms, it can lead to decisions that benefit a few individuals rather than the community as a whole. Without checks and balances, decisions may be made that prioritize personal interests over the best interests of homeowners.

3. Conflicts of Interest: If HOA board members have personal financial interests tied to certain decisions, there's potential for conflicts of interest. These conflicts can arise when board members benefit financially from particular contractors, vendors, or projects the HOA engages with.

4. Mismanagement or Incompetence: Sometimes, mismanagement or incompetence in financial matters can lead to suboptimal decisions. These decisions might inadvertently appear as if they're serving private interests, when in reality they're the result of poor financial planning or execution.

5. Inadequate Communication: When the HOA board fails to effectively communicate the reasons behind financial decisions, it can lead to misunderstandings and suspicions. Homeowners may wrongly assume that decisions are being made to serve private interests rather than the community's needs.

6. Lack of Homeowner Participation: If the homeowners are not actively involved in the decision-making process or if the board is unresponsive to homeowner input, it can create an environment where homeowners are more likely to assume the worst about the board's intentions.

7. It's worth noting that responsible HOA boards prioritize their fiduciary duty to the community. They aim to maintain healthy reserve funds to cover future maintenance, repairs, and unexpected expenses. These funds ensure that the community's property values are preserved and that residents' investments in their homes are protected.

If homeowners have concerns about financial practices or the management of reserve funds, it's important to address these concerns through proper channels. This might involve attending HOA meetings, communicating directly with the board, requesting financial reports, and, if necessary, electing new board members who are committed to transparency, accountability, and the overall well-being of the community.

Regenerate